New mortgage stress test regulations

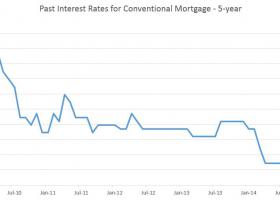

Starting January 2018, all uninsured mortgage borrowers will need to qualify at either the Bank of Canada’s five-year benchmark rate (currently 4.89 percent), or at their contract mortgage rate, plus an additional 2 percent. The move comes a year after the OSFI implemented the stress test for insured mortgages, which seemed to do little to cool Ontario’s red-hot housing market.

Now, the test will affect a much broader range of home buyers, at a time when the real estate market is still dealing with the effects of Ontario’s Fair Housing Plan — national sales rose at only 2.1 percent in September, while the national price of a home was up 2.8 percent.

Office of Superintendent of Financial Institutions (OSFI) is an independent agency of the Government of Canada that reports to the Minister of Finance. It was created to contribute to public confidence in the Canadian financial system. OSFI is the sole regulator of banks and the primary regulator of insurance companies, trust companies, loan companies and pension plans in Canada.

The new “stress test” rule will decrease buying power by approximately 20 percent or more for homebuyers who are applying for a conventional mortgage. For example, if a buyer qualifies for a maximum mortgage amount of $500,000 with a down payment of 20 percent or higher today, the amount will decrease. On or after January 1, 2018, they may only qualify for an approximate mortgage amount of $400,000 or less with a down payment of 20 percent or higher. The new mortgage rules will force many homebuyers to settle for cheaper homes or squeeze some out of the housing market altogether.

The next amendment to B-20 is for conventional lenders to clearly define a ‘non-conforming’ loan. In the past, lenders had some flexibility when faced with deficiencies in income, credit, or security. OSFI now expect lenders to have a clearly defined set of parameters where they identify what is non-conforming. It is expected that this change will result in fewer exceptions to lending guidelines and less common-sense lending, this will affect self-employed people the most.

In addition to the stress test, the new rules would require lenders to have more scrutiny around the loan-to-value ratio of the loans they give out, to ensure they are not giving out mortgages that are too large compared to the underlying value of the home.