Mortgage Default Insurance - What it is and isn't

Mortgage default insurance (sometimes called mortgage loan insurance) protects the mortgage lender in case you are not able to make your mortgage payments. It does not protect you.

You must pay for mortgage default insurance if your down payment is less than 20% of the purchase price of your home. This is called a high-ratio mortgage. Your mortgage costs will be higher if you need to get mortgage default insurance.

The maximum amortization period is 25 years for mortgages with mortgage default insurance.

Mortgage default insurance is only available for high-ratio mortgages if the purchase price of the home is less than $1 million.

If you can put at least 20% of the purchase price of your home as a down payment, you will have what is called a conventional mortgage. In this case, mortgage default insurance is generally not required. There are exceptions to this - for example, where your salary is not paid on a regular basis.

Who offers mortgage default insurance?

Mortgage default insurance is provided by insurers such as:

- Canada Mortgage and Housing Corporation (CMHC)

- Genworth Financial

- Canada Guaranty Mortgage Insurance Company.

How much are the premiums?

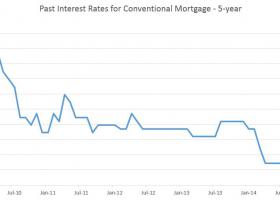

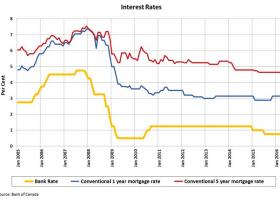

The premium—that is, the cost of mortgage default insurance—will vary depending on the down payment: the bigger your down payment, the lower your mortgage default insurance premium. Usually, mortgage default insurance premiums vary from 0.6% to 3.35% of the borrowed amount.

The premium can be added to your mortgage loan and included in your mortgage payments, or you can pay for it upfront in a lump sum. If the premium is added to your mortgage, you will pay interest on it at the same interest rate you pay on the principal amount of your mortgage.

0.25% premium surcharge on the above percentages can be added for every five years added to the amortization period beyond 25 years. There is no reduction if the amortization period is less than 25 years.

How to minimize mortgage default insurance

There is only one way to minimize your mortgage default insurance: increase your down payment as a percentage of your home price. To do this, you either have to increase the amount you put down or purchase a less expensive home. Examining the first option, you may want to consider additional sources for your down payment, such as a gift from a family member or, if you are a first-time homebuyer, a tax-free withdrawal from your RRSP.

So why not default?

The simple answer: Because you could still be on the hook for a portion of the original mortgage.

Under Canadian law insurance companies can legally come after you to replace any lost funds due to the foreclosure of your home—it’s called subrogation, and it’s a well-used legal tactic where the insurance company will try and recoup some or all of its losses for a paid out claim.

Many homeowners have no idea what transpires when they can’t pay their mortgage. An unknown number believe there’s a Canadian equivalent of jingle mail, (that’s the sound an envelope full of house keys makes when you mail it back to the bank). Large numbers of Americans, their houses underwater and unable to service their borrowing, just moved out and sent the keys back, or left them on the kitchen counter after receiving foreclosure notices.

However, most US states (39 of them) are just like most Canadian provinces: you can’t walk, the banks or the insures may come after you.

Technically, there are ‘recourse’ and ‘non-recourse’ mortgages. Canada is a country where the former applies (with the exception of Alberta), which means once you sign up for a mortgage you will never be rid of it unless you pay it off over time or through the proceeds of a sale.